The Investment Office Playbook - What Managers Don’t See

It happens hundreds of times a day.

A money manager walks into the office of a prospective investor. They’ve never been more confident: a long track record of success, stellar short-term results, an ideal strategy for the times, and a first-rate team to execute.

They never see it coming.

Five dreaded words go unstated as the manager wonders why the check never comes:

“It’s not you, it’s me.”

New investment relationships start when the manager fits into the allocator’s playbook, not the other way around. Managers often only see the game from their perspective. What happens on the other side of the field significantly influences the likelihood of a new allocation.

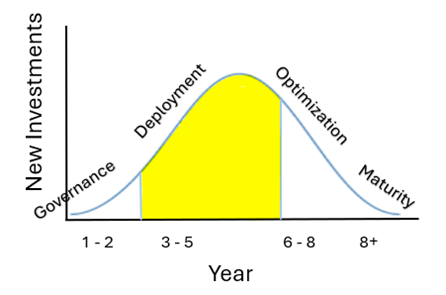

The investment office playbook takes place over four seasons – governance, deployment, optimization, and maturity. The seasons repeat each time a new CIO takes the helm. Other rules influencing investment activity include fund flows to the investment office and the CIO’s tenure in the seat.

The following chart displays the investment office playbook under a new CIO.

- Governance. A CIO comes into a new pool of capital and spends the first year or two creating the playbook for how they will operate and invest.

- Deployment. The investment office selects its roster of managers and puts money to work.

- Optimization. The team fine-tunes the portfolio, corrects mistakes, and upgrades the roster of managers.

- Maturity. The investment office patiently lets its all-star managers compound capital. Any new allocation must replace an existing one.

The deployment and early optimization seasons are the golden period for managers to approach an investment office. In the governance and maturity stages, managers are rarely invited on the field.

I’ll describe the playbook in some more detail.

Governance

It starts with a new pool of capital. Australian Superannuation Funds are around twenty-five years old; the Chan Zuckerberg Initiative investment organization is five, and new family offices launch every year.

Newly wealthy families or newly created institutions hire a CIO, who spends the first year or two preparing the investment strategy. This period includes creating an investment policy statement, recruiting a team, and determining how to allocate capital. Few new investments in funds occur during this time and those that do arise from high-conviction past relationships. No matter how strong a manager’s credentials may be, they are unlikely to win a mandate from an investment office during the governance stage.

Deployment

The next few years are the golden period for a manager to earn an allocation. After governance is complete, the CIO spends 2-4 years implementing the strategy. This is the most exciting and active period for the newly constituted investment office. Their eyes are wide open to opportunities, and great investment ideas in line with their strategy will find a spot on the roster.

Optimization

In the next season, the investment office will work to improve the quality of the portfolio. Money invested in the deployment stage will come with mistakes. David Morehead, CIO at Baylor University, believes that only 70% of his initial decisions were correct.[1] It took him another 2-4 years to rotate the remaining 30% into better ideas. That 30% will also have a 70% hit rate, so David has a few more years of making changes with a smaller proportion of the endowment to get to a steady state.

Maturity

When the optimization stage is complete, the investment team enters the mature season. Around eight years into their tenure, the CIO has built a portfolio that (mostly) lets them sleep at night. Any new allocations to managers face severe competition for capital. New managers approaching the investment office may be outstanding, but they must replace an existing player on the field to find a place in the allocator’s roster.

Many allocators pride themselves on being long-term partners to their managers. Their identity is tied to that behavior, which makes the hurdle for a new manager to replace an existing relationship much higher. That’s a wonderful characteristic if you are a manager in the portfolio. Not so much if you’re on the outside looking in.

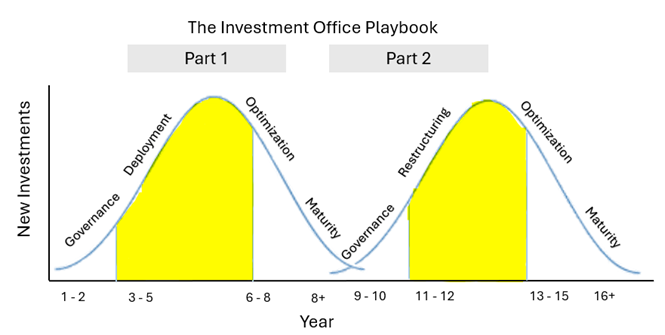

Part Two of the Investment Office Playbook

The mature season can last many years. Theoretically, it should last as long as the duration of the assets. Endowments, foundations, and sovereign wealth funds have perpetual time horizons – that’s a long time!

But that’s not what happens. The members of the investment office do not live forever, and their career path rarely aligns with the playbook of the investment office. Ana Marshall pointed out on the Capital Allocators podcast that the investment team that gets an organization to the mature season may not be the right team to keep them there.[2] Similarly, a CIO may look to play a different game by taking on a new challenge at a different organization.

When a new leader takes charge in the investment office, Part Two of the playbook begins and repeats a similar arc to Part One.

- Governance. The new CIO refreshes the governance and strategy in their image. This process takes a similar 1-2 years to the Governance season in Part 1.

- Restructuring. Over the next 1-2 years, the CIO may turn over the manager roster as they make their mark on the portfolio.

- Optimization. The CIO encounters mistakes in their decisions and finds better opportunities than they initially pursued, leading to more turnover in the manager roster.

- Maturity. After 5-8 years, the investment office again enters the mature season.

Part 2 is rarely the end of the game. In my podcast conversation about Carnegie Corporation of New York, Ellen Shuman, Kim Lew, Meredith Jenkins, and Alisa Mall discuss three transitions in leadership at Carnegie and three at other institutions where they took the helm after leaving Carnegie. Each instance had unique features, yet each also fit into the investment office playbook.

Deepening the Playbook – Shape of the Curve

The flow of funds to an investment office influences the pace of investment allocations during each season. Investment offices receiving inflows, like those overseeing multi-family offices or sovereign wealth funds, may have a continuing need for deployment through the optimization and mature phases. Offices with steady outflows, like foundations and legacy single-family offices, may have a shorter deployment phase and even more intense competition for capital. Other offices, like OCIOs or fund of funds, are one step removed from the asset owner and have less control over funds flowing in or out of their portfolios.

Another Winning Strategy – Investment Office Duration

The tenure of a CIO is correlated with investment success. League tables of allocators (however annoying and irrelevant they may be) almost always show that investment offices with the longest-standing CIOs deliver the best performance over the long term. Yale, MIT, and Princeton all had one thing in common: long-serving leadership.

The investment office playbook explains this dynamic. If it takes 5-8 years for a CIO to reach optimization and maturity, then any organization whose CIO leaves before that time never gets a chance to pursue continuous improvement from an optimized portfolio. It is rare to see a sophisticated co-investment program, direct management of select assets, or niche and tactical opportunities implemented by an investment office that hasn’t reached the mature season.

I joined the Yale Investments Office seven years after David Swensen became CIO. He had built a roster of incredible managers from top to bottom. It was a perfect time for me to learn the ropes and work on adding value through direct investments, secondaries, and one-off opportunistic strategies, but it was not a time for the active pursuit of new manager relationships. I can only imagine the incremental improvements David made over the quarter century after I left, each widening Yale’s advantage over its peers.

It’s Not You, It’s Me

For a manager seeking a new allocation, it’s usually not about you. Managers who learn the playbook of the investment office are best prepared to understand when the time is right to maximize their chances of making the allocator’s roster.